There Was Documentation, But the Receivable Was Not Real: Why Substance Verification Matters in the Imported Auto Parts Receivables Fraud Case

- May 6

- 3 min read

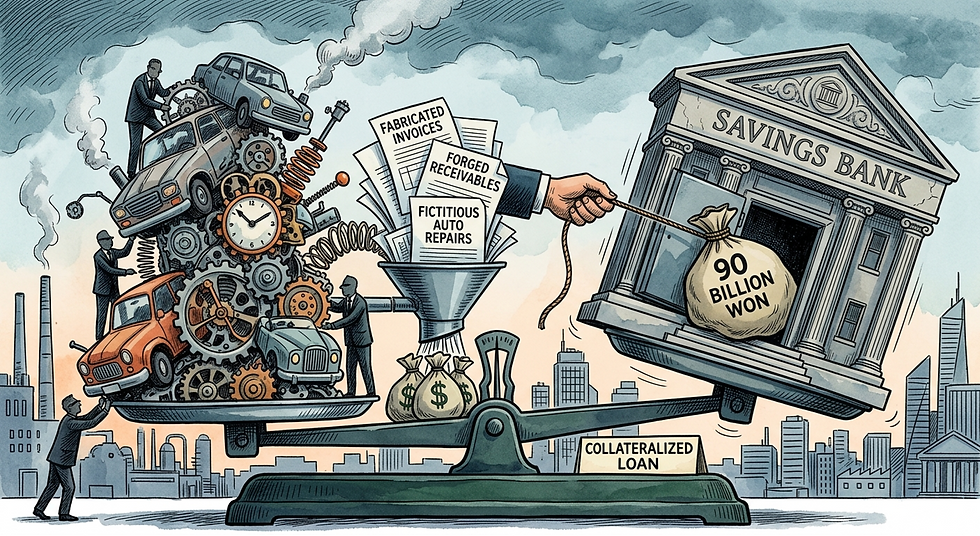

The recently reported case of fraud involving loans backed by receivables for imported auto parts shows clearly that, in financial fraud, what matters is not simply the existence of documentation, but verification of what that documentation actually represents.

At the center of this case was a scheme in which documents that could be generated through an automobile repair cost estimation system were packaged as if they were confirmed receivables tied to future insurance payments, and then used to obtain financing from financial institutions. According to the reports, the scheme allegedly exploited both the high unit prices of imported auto parts and the general difficulty of validating them. It involved making it appear as though expensive imported parts had been supplied even when they did not match the actual accident vehicle or repair details, or in some cases fabricating receivables altogether.

What is especially notable about this case is that the fraud was not built entirely on imaginary numbers. Rather, the parties appear to have taken documents that already existed within a real industry process involving auto insurance, repair work, parts supply, and cost estimation systems, and distorted their meaning. In other words, while there appeared to be system-generated documents and parts transactions on the surface, those documents did not in fact guarantee the substance of the receivables being pledged.

Another important aspect is the appearance of the supply chain and transaction structure. According to the article, multiple SPCs were used to create false or inflated receivables. While each individual transaction may have looked legitimate on its own, the overall network suggests the possibility that the ultimate borrower or the true source of the receivable was connected behind the scenes.

From a practical perspective, cases like this are easy to overlook because they create a false sense of comfort: there is a document generated by a system, and it appears to represent money that will be paid by an insurer. Yet in reality, cases like this often involve multiple red flags appearing together, such as the following:

• Whether lending exposure to a particular asset class has become excessively large relative to industry common sense

• Whether documents that are no more than repair estimates are being treated as if they were confirmed receivables

• Whether the accident vehicle information is consistent with the brand, item type, and unit price of the parts claimed

• Whether identical or similar SPC structures appear repeatedly

• Whether transactions are concentrated around specific parts suppliers, repair shops, or intermediary channels

• Whether receivables with similar amounts, similar descriptions, and similar document formats recur repeatedly

• Whether there was any independent verification of the actual insurance claim status or payment confirmation

• Whether the overall portfolio size remains realistic even if individual transactions appear plausible

Fraud of this type is difficult to identify by reviewing a single document in isolation. Structural anomalies become visible only when multiple factors are reviewed together, including the type of pledged document, the actual status of the claim and payment process, consistency between the vehicle and the parts supplied, concentration within the transaction network, and whether total exposure is reasonable relative to market reality.

Recent cases make one point clear. Financial fraud no longer relies only on crude forged documents. It is evolving into a form that uses real systems and real documents embedded in actual industry processes, making transactions appear legitimate on the surface while distorting what those documents truly mean. That is why CEOs, CFOs, and internal audit leaders need to ask not simply whether documentation exists, but what legal right and expected cash flow that documentation actually represents.

From this perspective, preemptive reviews by companies and financial institutions also need to become more sophisticated. Even with existing data and currently available rules, it is still possible to identify a meaningful portion of similar warning signals, such as:

• Transactions or receivable patterns supported by documentation but lacking substance

• Concentration patterns involving specific counterparties or supply chain channels

• Unusually large exposure concentrated only in a particular product category

• Repeated use of near-duplicate documents or descriptions

• High-value transactions involving counterparties with weak business substance

• Unusual exposure concentration that does not align with industry reality

GRAM Radar is a data-driven Financial Risk Quick Scan designed from this perspective. Using financial and transactional data, it helps organizations assess weak-substance transactions, concentration around specific counterparties, category-level anomaly concentration, repeated near-duplicate documentation patterns, and weaknesses in counterparty substance. Rather than viewing recent cases simply as someone else’s problem, it may be far more practical and cost-effective to first examine whether similar signals already exist within your own company or financial portfolio.